Assigns weights that decay in three different directions as determined by

the combination of weights_exponential(), weights_seasonal(), and

weights_seasonal_decay().

Arguments

- alpha

The smoothing factor passed to

weights_exponential()that determines the overall monotonic exponential weight component- alpha_seasonal

The smoothing factor passed to

weights_seasonal()that determines the exponential weighting within a seasonal period- alpha_seasonal_decay

The smoothing factor passed to

weights_seasonal_decay()that determines the exponential weighting of the seasonal periods- n

The number of weights to create; this is usually equal to the number of observations in a time series

- period_length

The length of the seasonal period to be modeled

Examples

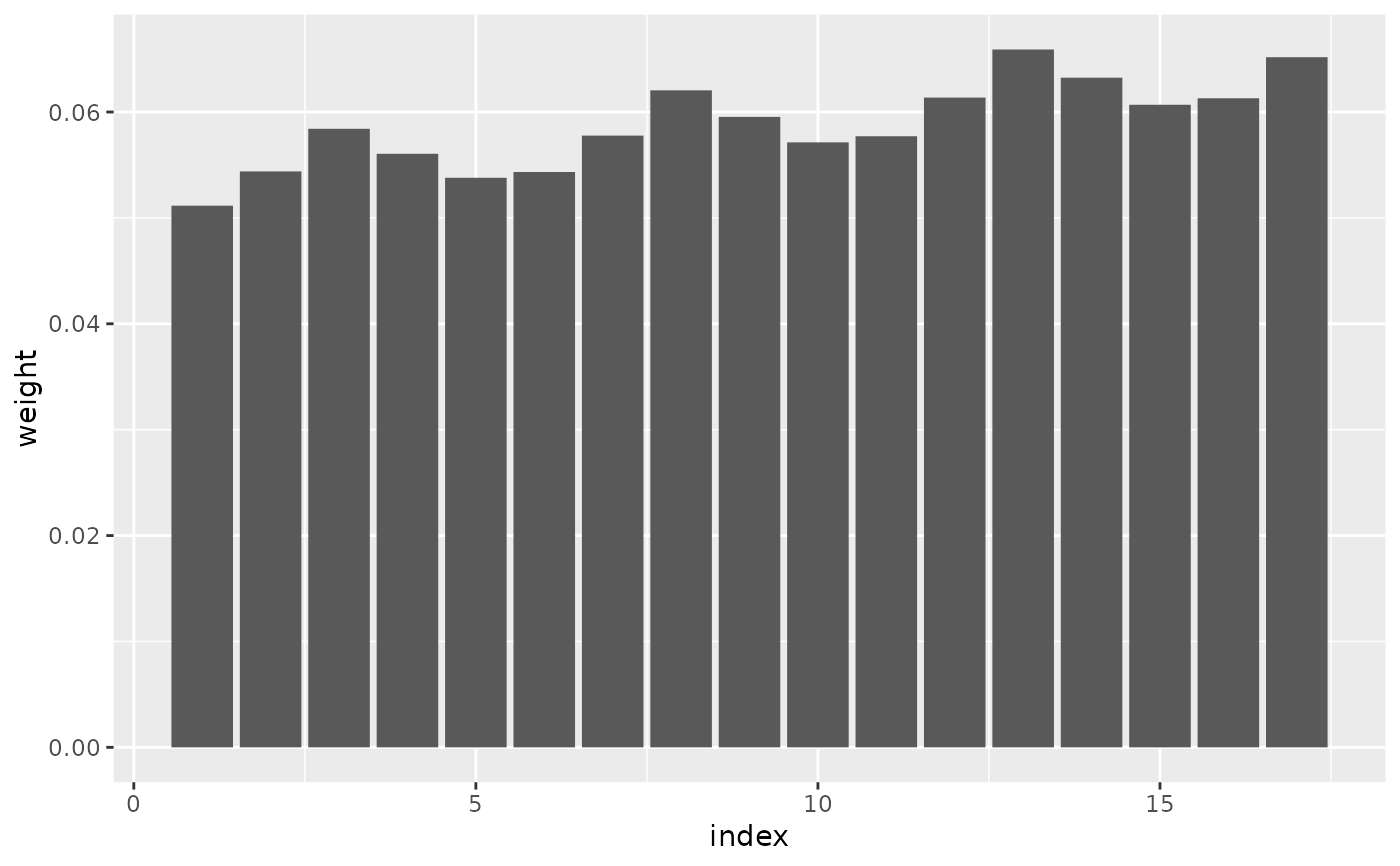

weights <- weights_threedx(

alpha = 0.01,

alpha_seasonal = 0.05,

alpha_seasonal_decay = 0.01,

n = 17,

period_length = 5

)

print(weights)

#> [1] 0.05115383 0.05439003 0.05841513 0.05605492 0.05379007 0.05433341

#> [7] 0.05777077 0.06204605 0.05953914 0.05713352 0.05771063 0.06136164

#> [13] 0.06590267 0.06323993 0.06068478 0.06129776 0.06517572

if (require("ggplot2")) {

ggplot2::ggplot(

data.frame(index = seq_along(weights), weight = weights),

ggplot2::aes(x = index, y = weight)

) +

ggplot2::geom_col()

}

# random walk forecast

weights_threedx(

alpha = 1,

alpha_seasonal = 0,

alpha_seasonal_decay = 1,

n = 30,

period_length = 12

)

#> [1] 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 1

# mean forecast

weights_threedx(

alpha = 0,

alpha_seasonal = 0,

alpha_seasonal_decay = 0,

n = 30,

period_length = 12

)

#> [1] 0.03333333 0.03333333 0.03333333 0.03333333 0.03333333 0.03333333

#> [7] 0.03333333 0.03333333 0.03333333 0.03333333 0.03333333 0.03333333

#> [13] 0.03333333 0.03333333 0.03333333 0.03333333 0.03333333 0.03333333

#> [19] 0.03333333 0.03333333 0.03333333 0.03333333 0.03333333 0.03333333

#> [25] 0.03333333 0.03333333 0.03333333 0.03333333 0.03333333 0.03333333

# seasonal mean forecast

weights_threedx(

alpha = 0,

alpha_seasonal = 1,

alpha_seasonal_decay = 0,

n = 30,

period_length = 12

)

#> [1] 0.0 0.0 0.0 0.0 0.0 0.0 0.5 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.5

#> [20] 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

# seasonal naive forecast

weights_threedx(

alpha = 0,

alpha_seasonal = 1,

alpha_seasonal_decay = 1,

n = 30,

period_length = 12

)

#> [1] 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 1 0 0 0 0 0 0 0 0 0 0 0

# last year's mean forecast

weights_threedx(

alpha = 0,

alpha_seasonal = 0,

alpha_seasonal_decay = 1,

n = 30,

period_length = 12

)

#> [1] 0.00000000 0.00000000 0.00000000 0.00000000 0.00000000 0.00000000

#> [7] 0.00000000 0.00000000 0.00000000 0.00000000 0.00000000 0.00000000

#> [13] 0.00000000 0.00000000 0.00000000 0.00000000 0.00000000 0.00000000

#> [19] 0.08333333 0.08333333 0.08333333 0.08333333 0.08333333 0.08333333

#> [25] 0.08333333 0.08333333 0.08333333 0.08333333 0.08333333 0.08333333

# random walk forecast

weights_threedx(

alpha = 1,

alpha_seasonal = 0,

alpha_seasonal_decay = 1,

n = 30,

period_length = 12

)

#> [1] 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 1

# mean forecast

weights_threedx(

alpha = 0,

alpha_seasonal = 0,

alpha_seasonal_decay = 0,

n = 30,

period_length = 12

)

#> [1] 0.03333333 0.03333333 0.03333333 0.03333333 0.03333333 0.03333333

#> [7] 0.03333333 0.03333333 0.03333333 0.03333333 0.03333333 0.03333333

#> [13] 0.03333333 0.03333333 0.03333333 0.03333333 0.03333333 0.03333333

#> [19] 0.03333333 0.03333333 0.03333333 0.03333333 0.03333333 0.03333333

#> [25] 0.03333333 0.03333333 0.03333333 0.03333333 0.03333333 0.03333333

# seasonal mean forecast

weights_threedx(

alpha = 0,

alpha_seasonal = 1,

alpha_seasonal_decay = 0,

n = 30,

period_length = 12

)

#> [1] 0.0 0.0 0.0 0.0 0.0 0.0 0.5 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.5

#> [20] 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

# seasonal naive forecast

weights_threedx(

alpha = 0,

alpha_seasonal = 1,

alpha_seasonal_decay = 1,

n = 30,

period_length = 12

)

#> [1] 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 1 0 0 0 0 0 0 0 0 0 0 0

# last year's mean forecast

weights_threedx(

alpha = 0,

alpha_seasonal = 0,

alpha_seasonal_decay = 1,

n = 30,

period_length = 12

)

#> [1] 0.00000000 0.00000000 0.00000000 0.00000000 0.00000000 0.00000000

#> [7] 0.00000000 0.00000000 0.00000000 0.00000000 0.00000000 0.00000000

#> [13] 0.00000000 0.00000000 0.00000000 0.00000000 0.00000000 0.00000000

#> [19] 0.08333333 0.08333333 0.08333333 0.08333333 0.08333333 0.08333333

#> [25] 0.08333333 0.08333333 0.08333333 0.08333333 0.08333333 0.08333333